Learning the basic dental insurance terminology and the most important terms for daily dental office management – is paramount to understanding how dental practices generate revenue and how profit is calculated.

If you’re part of the administrative team in a dental practice, or maybe you’re the doctor getting in to practice ownership – this video is going to be super helpful for you in understanding important dental terminology such as Gross production, Net Production, Adjustments, Collections, Write-offs, In-network vs out of network, deductible, copays, etc.

This is NOT meant to be a comprehensive video on ALL the insurance terminology – although I’ll cover a few that you’ll need to know to understand how things fit together.

In the end of the video, I bring together all the things we’ve discussed by showing you an appointment schedule with patient appointments. – so make sure to stick around to the end to understand how to actually APPLY these definitions for what you need on a daily basis!

Why is it important to understand the Dental Insurance terminology?

If you’re the practice owner, you’ll need to understand what affects your bottom line.

If you don’t understand the basics, your may seem busy in your practice because there’s lots of appointments – but it’s NOT a productive schedule.

If you’re an office manager or part of the front desk administration – if you understand the principles, you’ll be able to apply it to most things that come your way on a daily basis.

Your Practice Management software may not do everything that you want – so there are times you’ll have to tweak how it works, but if you understand the bottom line numbers – you will be able to do this easily.

When you run reports to figure out doctor production & income, or Aging report – meaning – how much money is owed by insurance and/or patients – if you don’t know your basics, it’s going to be difficult for you to understand what you’re reading on the reports.

If you don’t understand the reports, it’s difficult to make data driven decisions that require you to take action to move the “needle forward” for whatever it is you’re trying to do in your practice.

In-network vs Out-of-Network

In-network

When you’re in-network with an insurance company, it means you’ve agreed to provide dental services at some negotiated rates. It also means you’re a Participating provider.

So what does that mean?

It means if you’re seeing a patient with MetLife Insurance and you’re an in-network participating provider, you cannot charge more than the MetLife fee for a procedure.

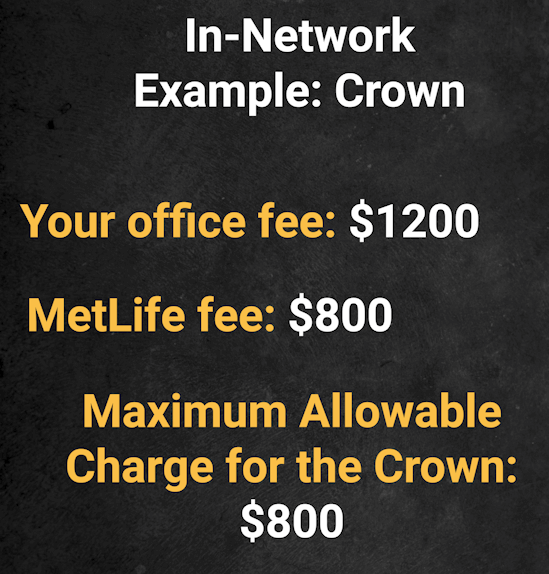

Here’s an example:

Patient comes in for a crown. Your office fee is $1200 for the crown. But if you’re in-network with Metlife, you’re obligated to follow their fee schedule.

The MetLife fee for that crown is, for example – $800. That means $800 is the Maximum-allowable charge for that procedure.

There are some exceptions to this and it varies by states, so you’ll want to check the rules.

What this is means is that – for instance, if the insurance has no coverage for bone graft – you may be able to charge upto your office fee. Again, this depends on the State your practice is in!

Otherwise, even though the insurance has no coverage for bone graft, you can only charge the patient up to the amount agreed to with that insurance.

Out-of-network

When you’re out-of-network, it means you’re NOT contracted with an insurance company, so you’re not obligated to accept the insurance fees.

You can charge upto your Office fee schedule for a procedure – and depending on the insurance plan, if it has out-of-network benefits, you can file a claim for a patient to receive out-of-network benefits to lower the patient’s out of pocket.

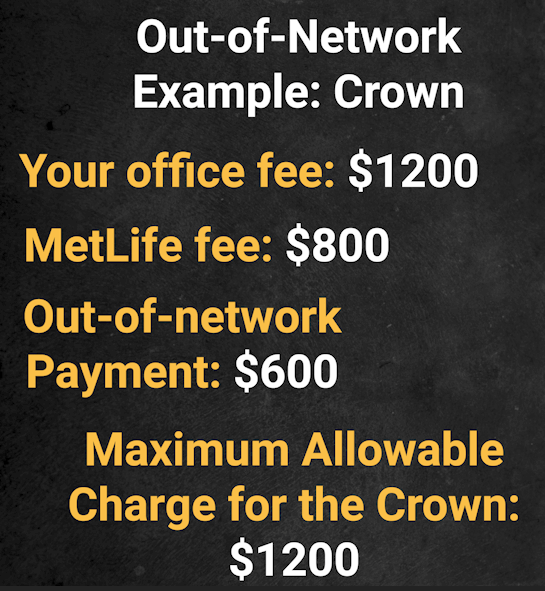

Here’s an example:

We’ll use the same example for the crown we discussed earlier. Let’s say your fee for the crown is $1200.

But you’re out-of-network with the patietn’s insurance, which is MetLife.

You may then file a claim with MetLife once the work is completed for the procedure and lets say MetLife pays $600.

Because you’re out of network, you’re allowed to charge the patient the difference between your office fee (which is $1200) and what the insurance paid ($600) – which makes the patient out-of-pocket $600.

Production / Gross Production

This is the $ amount produced for a procedure – which is equal to whatever your office fee is for that procedure.

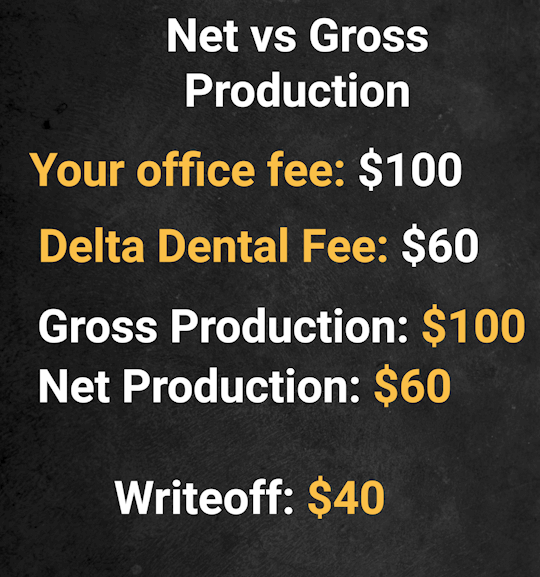

If you do a prophy for a patient, and your office fee for that procedure is $100 – then your Gross production for that procedure is $100.

If you take insurance in your practice, the gross production is NOT the most important number since in-network plans require you to follow THEIR fee schedule as I discussed earlier.

So in that case, when it comes to production – the important term you need to understand is NET PRODUCTION.

Net Production

Net production is really important if you’re going to accept insurance in your practice.

So in the above example, I told you that if your office fee for prophy is $100 – then your Gross production is $100.

But if you are in-network with, for instance, Delta Dental – and the Delta Fee is $60 for prophy – then your Net Production is $60 after writing-off $40.

Write-offs

Write-off is the difference between your Office fee and the insurance fee. So in the above example, your office fee is $100 and your Delta Fee is $60 – so you’re writing-off $40! – or whatever insurance doesn’t cover.

Collections

This is the total amount of money you collect from patients directly, and/or from insurance companies for claims you’ve filed

Payments can be in the form of:

- Check

- Credit Cards

- EFT (Electronic Fund Transfer – from Insurance Companies)

- Payments from 3rd party Financing companies (CareCredit, Lending Club, etc.)

Example

Let’s say you saw a patient today who has no insurance – which means they’re fee for service. You did a crown on #11 and your office fee is $1200.

When this patient is checking out at the front, and they make the payment in full of $1200 – then your collection is $1200 for that patient.

Let’s say you have an agreement with the patient where you allow them to pay half at crown prep and half at insert – which means on prep date, they pay $600. Your collection on that day for that patient is $600.

So your Gross production is $1200, but your collection is $600.

Deductible

For insurance patients, this is what the patient has to pay out of pocket before the benefits kick in.

Whenever the patient has any work done – filings, crowns, perio, etc. – the patient’s deductible kicks in.

There are plans which also require patient to pay a deductible even for preventive services like cleaning, exams, and xrays.

This is what you have to find out when your team is verifying the patient’s insurance.

Example

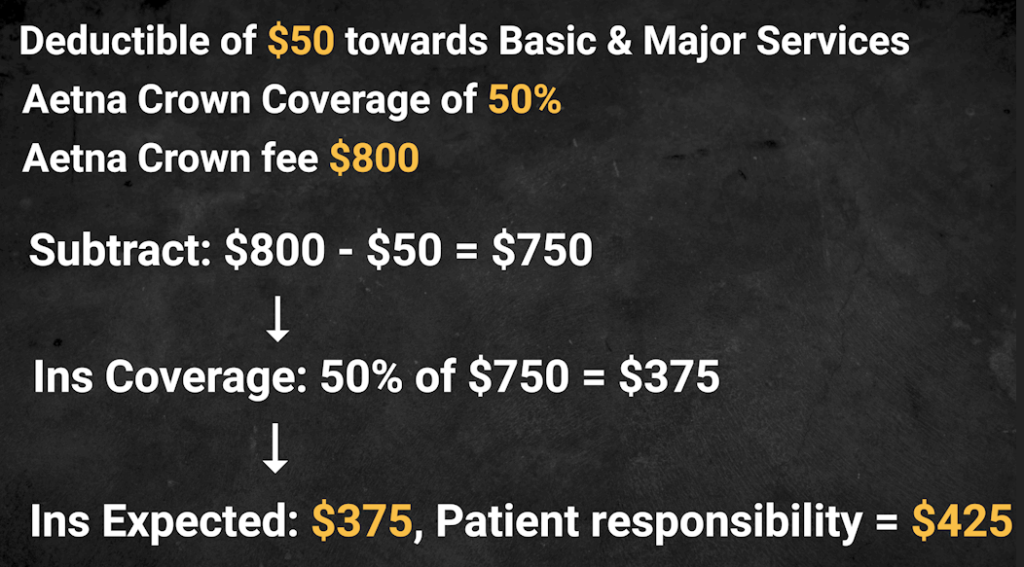

Let’s look at an example of how deductible is used when calculating a patient’s co-pay:

Let’s say a patient’s plan has a deductible of $50 towards basic and major services, and for this example, let’s say their crowns are covered at 50%.

Let’s say the insurance is Aetna and the Aetna crown fee is $800.

So the way the patient out of pocket is calculated is the following:

You first subtract the deductible from the Insurance fee.

$800 – $50 (deductible) and then 50% of that is what the insurance will pay.

50% of 750 is $375.

So the insurance expected amount is $375, which makes the rest ($800-375) patient’s responsibility: $425

Understand this concept!

Don’t worry about how this is set up in a practice management software yet, or how it’s done for big treatment plans.

What’s important here is that you UNDERSTAND how the patient out of pocket is calculated.

Adjustments

Adjustments are manual changes that you apply to a patient’s account.

This can be in the following forms:

- A discount

- manual write-off for an amount insurance is not going to pay

- Administration fee charges

- Sales tax on retail items you may be selling (Electric toothbrushes, whitening products, etc.)

When it comes to Open Dental’s built in reports on production, the adjustments will be take into account when calculating your Net Production.

Let’s say your Total net Production (after considering all write-offs) for all patients on schedule today is $4000.

However, your manager made an adjustments on a patient account today from a procedure done a month ago in the form of a discount of let’s say $300.

Then the Net Production for today is going to be $4000-$300 = $3700.

It’s important you understand this, so you don’t get confused when you’re looking at reports to understand your daily / monthly or annual numbers!

Putting it all together

Watch the video above to see how these terms are used on a daily basis when looking at an example appointment schedule.